{kind=link}

n the realm of financial planning, one essential aspect often overlooked is non-life insurance. While life insurance understandably garners significant attention, non-life insurance, also known as property and casualty insurance, is equally critical for safeguarding against unforeseen events. These policies cover a broad spectrum of risks, including damage to property, liability for injuries, and legal expenses. Among the key players in this arena are non-life insurance companies, dedicated to providing protection and peace of mind to individuals and businesses alike.

Understanding Non-Life Insurance Companies

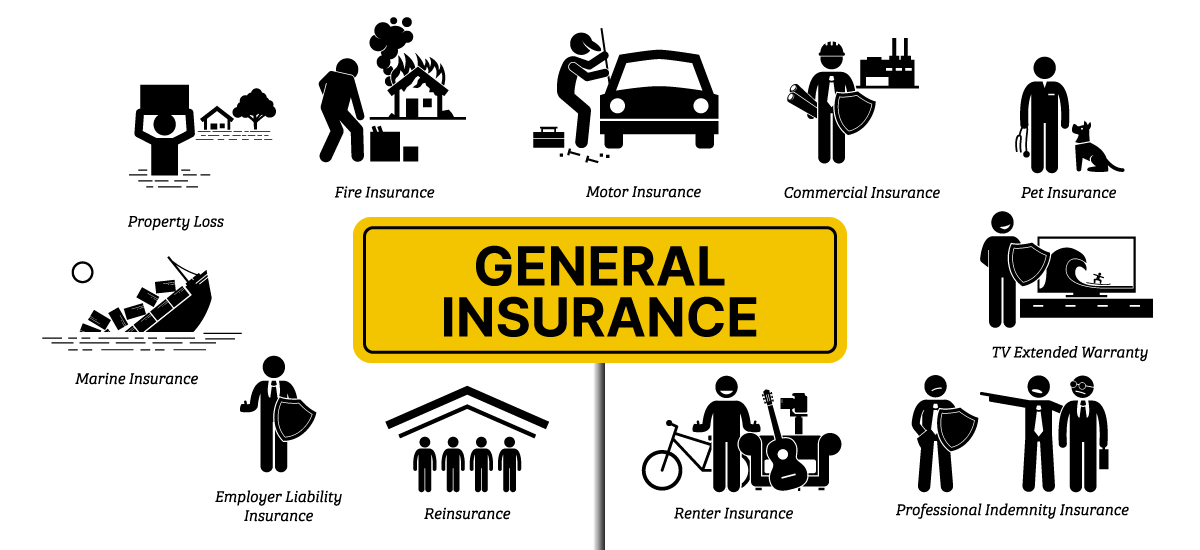

Non-life insurance companies specialize in offering policies that protect against losses other than those involving life insurance. They provide various types of coverage, including automobile, homeowner’s, renter’s, and commercial property insurance, as well as liability insurance for individuals and businesses. These companies assess risks, determine premiums, and manage claims related to property and casualty insurance.

FAQs About Non-Life Insurance Companies

1. What types of coverage do non-life insurance companies offer?

Non-life insurance companies offer a wide range of coverage options, including:

- Automobile insurance: Protection against financial loss in the event of an accident, theft, or damage to a vehicle.

- Homeowner’s insurance: Coverage for damage to a home and its contents, as well as liability for injuries that occur on the property.

- Renter’s insurance: Protection for personal belongings and liability coverage for renters.

- Commercial property insurance: Coverage for buildings, equipment, inventory, and other property owned by businesses.

- Liability insurance: Protection against claims for bodily injury or property damage caused by the policyholder.

2. How do non-life insurance companies determine premiums?

Premiums for non-life insurance policies are typically based on various factors, including the type and amount of coverage, the insured’s risk profile, the value of the insured property, and the likelihood of filing a claim. Insurers use actuarial data and statistical models to assess risk and calculate premiums accordingly.

3. What should I consider when choosing a non-life insurance company?

When selecting a non life insurance company, consider the following factors:

- Financial stability: Choose a company with a strong financial rating to ensure its ability to pay claims.

- Coverage options: Look for a company that offers the types of coverage you need, with customizable options to suit your specific requirements.

- Customer service: Evaluate the insurer’s reputation for customer service, responsiveness, and claims handling.

- Pricing: Compare premiums from multiple insurers to find the most competitive rates without compromising on coverage quality.

4. How can I file a claim with a non-life insurance company?

To file a claim with a non-life insurance company, follow these steps:

- Contact your insurer as soon as possible to report the incident and initiate the claims process.

- Provide accurate and detailed information about the loss or damage, including photos, receipts, and any relevant documentation.

- Cooperate fully with the insurer’s claims adjuster and provide any additional information or documentation requested.

- Keep records of all communications with the insurer and any expenses incurred as a result of the claim.

In conclusion, non-life insurance companies play a crucial role in protecting individuals and businesses from financial losses due to unforeseen events. By understanding the offerings and processes of these insurers, consumers can make informed decisions to secure the coverage they need for peace of mind in an unpredictable world.